The final invoice represents the result of commercial negotiations between the foreign supplier and the importer. It is a standardized commercial document that gives rise to an accounting record. It differs from the “pro-format” invoice since the latter is an estimate presented in the form of an invoice without providing any accounting value.

The final invoice must contain all the information necessary for the smooth running of the transaction, namely:

The contracting parties and their contact details;

The designation of the product;

The unit price and quantity of the product;

The global price and the settlement currency according to the chosen incoterm;

Guarantees and force majeure in the event of an unforeseeable event…

Le modèle de la facture définitive

The certificate of origin

|

All economic operators must be able to prove the origin of their imported products during customs clearance. In other words, it is the proof of “nationality” of the product which allows the economic operator to benefit from the preferences provided for by bilateral or multilateral conventions and agreements, the establishment of foreign trade statistics or for the application of specific regulations such as health and phytosanitary measures.

The processing shall be classified as substantial where,

one or more of the following criteria are met:

The product obtained is classified in a four-digit tariff heading of the Harmonized System (HS) different from those of the materials used to obtain it.

The local added value achieved in obtaining the product in question which is equal to or greater than 40% of the ex-factory price of the product in question.

The product obtained has undergone a certain number of workings or transformations in accordance with the regulations in force.

The importer or his authorized representative shall be required to submit to the customs authorities the certificate attesting the origin of his imported products.

It should be noted that certificates of origin are classified into two categories:

They concern commercial exchanges which are not governed by preferential tariff agreements, when the criteria of origin as defined within the framework of preferential relations are not satisfied, re-export of foreign products or when the certificate of origin is required as documentary evidence in addition to the conventional certificate of origin.

They are used for commercial exchanges governed by bilateral or multilateral preferential tariff agreements with a view to reducing or exempting customs duties and taxes with equivalent effect. Each agreement binding Tunisia with its partners defines its own rules of preferential origin.

Conventional certificates of origin

Certificate of origin established within the framework of bilateral agreements between Tunisia and certain Arab countries (Morocco, Egypt, Jordan, Libya, Kuwait, Algeria)

Certificate of origin for the movement of goods for the export of originating products to the European Union (EUR1 certificate)

Certificate of origin of movement of goods for the export of products in the PANEUROMED zone (EUROMED certificate)

Common Market for Eastern and Southern Africa COMESA Free Trade Area Certificate of Origin

Veterinary health control

|

The applied framework is governed by law 99-24 of March 9, 1999, relating to veterinary health control at import and export. This control is carried out at crossing points with customs offices by sworn veterinarians.

Imported animals and animal products must be accompanied by health documents issued by the official veterinary authorities of the exporting country attesting to their good health, their wholesomeness as well as their conformity with the sanitary and hygienic requirements in force in Tunisia.

Veterinarians mainly check the documents accompanying the animals and animal products as well as the identity check by visually checking the concordance between these documents and the animals/animal products.

If it turns out to be non-compliant with documentary and identity checks, the animals and animal products will be returned or destroyed if the reshipment outside Tunisian territory is impossible.

In case of suspicion, veterinarians can carry out a physical check of animals and animal products via an examination or sample collection. In case of non-compliance with the results of the analysis, the seizure, the slaughter of the living animals and the destruction of the animals and animal products will be carried out after authorization from the territorially competent judge.

Phytosanitary control on import

|

Phytosanitary import control aims to prevent the introduction and spread of dangerous harmful organisms which can cause direct or indirect losses on the national plant heritage. It concerns plants (live plants and living parts of plants including seeds and fruits) and plant products (unprocessed products of plant origin).

The procedure is carried out by the phytosanitary control service within the border posts (ports, airports, land crossing points).

Plants, parts of plants and plant products imported into Tunisia must be accompanied by a phytosanitary certificate in accordance with the model established by the International Convention for the Protection of Plants (written in Arabic, French or English).

If the exporting country is not the country of origin, the plants, parts of plants and plant products must be accompanied by a phytosanitary certificate for re-export conforming to the model established by the International Plant Protection Convention to which will be annexed the original or a copy of the original phytosanitary certificate certified by the exporting country.

If the exporting country has not required a phytosanitary certificate for the import of consignments intended for re-export to Tunisia, these consignments must be accompanied by a phytosanitary certificate issued by the competent services of the country of re-export, in accordance with the model established by the International Convention for the Protection of Plants, certifying that the consignment has not undergone any modification during its storage that could make it non-compliant with Tunisian phytosanitary requirements.

The certificate drawn up no earlier than 14 days before shipment must certify that the shipment has been officially examined and found free from harmful organisms covered by the decree of 31 May 2012, establishing the list of quarantine organisms. This certificate also declares to respect the specific requirements of 19 families of plant products listed in the decree of the Minister of Agriculture of May 28, 2013, setting the phytosanitary requirements as well as the methods of control of plants and plant products imported into Tunisia.

Furthermore, the same text authorizes the import without presentation of a phytosanitary certificate or phytosanitary inspection the introduction of 6 families of plants or plant products, with the exception of those covered by the decree of the Minister of Agriculture of 31 May 2012 establishing the list of plants and plant products whose entry into Tunisian territory is prohibited, these plants or plant products concern:

in small quantities and for personal consumption with the exception of seeds.

If the imported product is non-compliant, it will be intercepted at the point of entry and may be subject to treatment, transformation, return or destruction, and this, according to the availability of the technique for the eradication of the organism concerned within pre-determined deadlines.

The technical control on import

|

Table A of this decree divides the groups of products subject to technical inspection on import according to the departments concerned, namely: Ministry responsible for trade, Ministry responsible for industry, Ministry responsible for health, Ministry responsible for agriculture , Ministry in charge of Communication Technologies and the Digital Economy.

Raw materials, semi-finished materials intended for the professional use of the importer within the framework of his industrial, agricultural, craft or tourist activity, also imported samples, advertising items for everyday use, goods intended for exhibitions and not intended for sale on the local market, imports from diplomatic missions, imports from the Tunisian red crescent, goods imported as a gift by administrations and public administrative establishments and returned goods.

These are the products on list A of the text of the decree and mainly concern final consumer products (cosmetics, food, shoes, toys, household appliances, etc.).

Based on a system of risk management and selectivity (related to the nature of the product in question, content of the file, history of the importer, warnings regarding the harmfulness of the product, etc.), each technical department concerned performs this type of control according to three ways:

Study of file with possibly a deposit of samples;

Study of file with control of the goods;

Study of file with control of the goods and taking of sample for analysis;

These are the products listed in List B of the text of the above-mentioned Order. This check shall be carried out by customs officials who shallverify at the time of customs clearance that the goods are accompanied by a certificate of conformity with the technical regulations concerning them issued by a body duly authorized for that purpose.

concerning the products of list C of the text of the decree mentioned above. This control is carried out by the technical department concerned and consists of verifying the conformity of the product with the requirements of a specification (approved by order of the Minister of Commerce and the ministers concerned). Similarly, the technical departments may take samples as part of the study of the file.

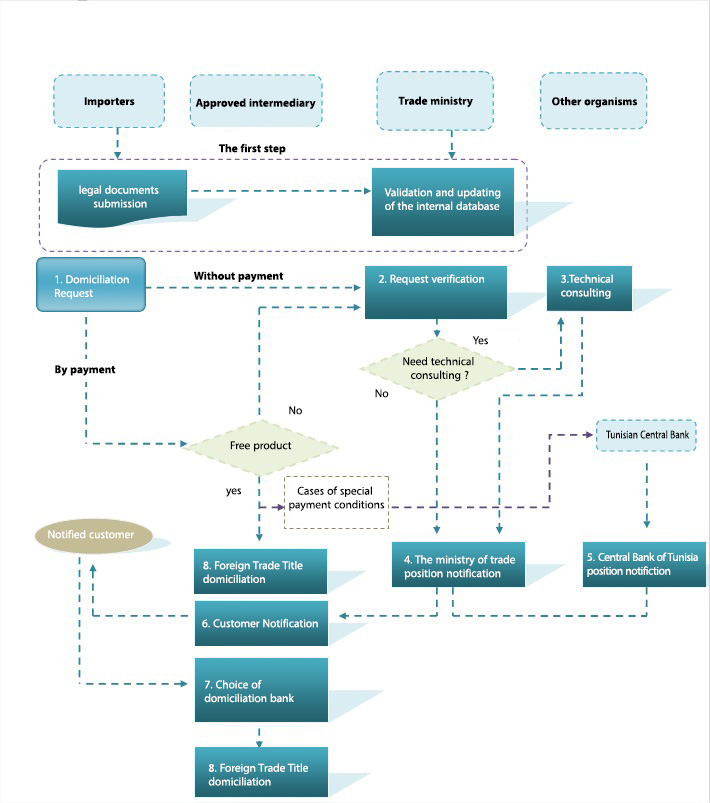

Bank domiciliation means the choice by a natural or legal person of an approved intermediary to carry out a transfer of foreign currency (in payment for an import or for another reason) or to send foreign currency in recovery of an export transaction.

Bank domiciliation

The bank domiciliation is made under cover of a TCE foreign trade document which is an administrative document personal to its beneficiary. It is called:

The bank domiciliation is made under cover of a TCE foreign trade document which is an administrative document personal to its beneficiary. It is called:

The direct debit request (accompanied by the commercial contract and any other document deemed necessary) is submitted to the authorized intermediary who verifies the content of the invoice and the NGP code of the product to be imported.

Request for authorization without payment: The file is transmitted directly to the Ministry of Trade and Export Development via the TTN application (without going through the approved intermediary) which decides on the latter by possibly transmitting it to another competent structure to technical advice.

The authorized intermediary must respect the regulatory change requirements and obtain the agreement of the central bank in the event that the importation provides for special payment conditions (provisions of the circular of the BCT to authorized intermediaries No. 94-14 of September 14, 1994).

Following a suitable decision from the Ministry of Commerce and possibly the central bank, the operator can proceed with the domiciliation of his foreign trade title, unless he claims to domicile his title with another approved intermediary.

As for the commercial invoice, its duration is fixed at 6 months from the date of its domiciliation. The importation can be made in a split way during the period of validity of the domiciliation of the foreign trade document.

If it is a product excluded from the freedom of foreign trade regime, the import authorization is transmitted under slip to the Ministry of Trade and Export Development.

Depending on the nature of the product, the Ministry of Trade and Export Development may forward this file to another competent authority for technical advice..

After obtaining the technical opinion, the Ministry of Trade and Export Development mentions its decision to the authorized intermediary who is then, responsible for transmitting this decision to the operator.

For the case of the first import operation of a product excluded from the freedom of foreign trade regime: a legal file must be filed with the Directorate General for Foreign Trade so that it can update its internal databases. This file contains an information sheet, the customs code, a copy of the license, the commercial register and the legal status relating to the importer.

The import authorization is valid for 12 months from the date of the decision of the Ministry of Trade and Export Development.

Domiciliation of the Foreign Trade Document

Pre-Import Surveillance

|

Article 30 of Law No. 98-106 of 18 December 1998 relating to import safeguard measures stipulates that, when it appears that the development in imports of a given product threatens to cause damage to national producers, the importation of this product may be subject to prior surveillance in accordance with the procedures laid down by the Order of the Minister of Commerce of 12 August 2004 establishing the procedures for surveillance prior to importation.

Surveillance prior to importation takes the form of an information sheet aimed at informing the Ministry responsible for trade, in advance, of the bank domiciliation of any import operation of products subject to this regime.

Import authorization

|

Despite the general rule of freedom to import, Article 3 of the law on foreign trade excludes from the regime of freedom of foreign trade all products relating to security, public order, hygiene, health, morals, protection of fauna and flora and cultural heritage.

However, these products may exceptionally be imported under cover of an import authorization granted by the Ministry responsible for trade. They mainly concern the following products:

Products imported under import authorization

Products excluded from the regime of freedom of foreign trade

Transactions carried out under the compensation regime;

Products benefiting from tax privileges under government decree no. 2015-2605 of 25 December 2015 on the modalities and procedures for granting tax advantages provided for in articles 31 and 75 of law no. 2015-53 of 25 December 2015, Finance Act for 2016;

Imports without payment

Products benefiting from a reduction in customs duties under tariff quotas;

Products subject to the warehousing or temporary admission procedures in the event of a financial settlement with foreign countries of the value of imported products if such products are subject to authorization under common law;

Sales of totally exporting companies, excluding those released for consumption within the framework of the 30% reserved for release for consumption on the local market for products excluded from the freedom of foreign trade regime;

Used or renovated products

Products benefiting from total or partial exemption from import customs duties within the framework of bilateral agreements and conventions concluded between Tunisia and other countries;

Imported products released for consumption under special regimes if they are subject to authorization under common law;

Imports without currency transfer;

Importation of certain hazardous chemicals;

Modes of transport and their particularities

|

In order to optimize the operations of transporting the goods to the customer, it is better to choose the most appropriate mode of transport by taking into account parameters such as the quantity of goods to be transported, the delivery time, the cost of transport, the distance to be covered and the security linked to the delivery of the goods. The table below shows the advantages and disadvantages for each mode of transport.

To complete an import procedure, it is necessary to have a customs code, which will be used by the operator as a unique identifier in the TTN foreign trade electronic counter. The latter is presented as the computer network that connects the various stakeholders in the procedures of foreign trade and transport in Tunisia.

The economic operator can file his request for the creation of a customs code at the customs office closest to his home or at the one-stop shop of the Agency for the Promotion of Industry and Innovation (APII).

The file contains the following documents:

The original of the certificate of registration in the national business register;

A request on a specific form to be collected from the nearest customs office or from the counter of the Agency for the Promotion of Industry and Innovation (APII);

A copy of the tax identity card legalized at the tax control office;

A copy of the declaration of existence certified with the tax control office;

A certificate of publication of the notice of creation of the company in the Official Journal of the Republic of Tunisia (in the case of a legal person);

A copy of the company’s status (in the case of a legal entity);

A copy of the national identity card of the applicant or the legal representative of the company

{kind=link}